It’s no secret that the vast majority of U.S. housing stock is in need of improvements — for reasons of comfort, safety, and health, but especially to address sub-par energy performance. To adequately tackle our climate imperatives, those home energy improvements must happen quickly and at scale. And yet, the upfront cost of meaningful home energy improvements is challenging, both for a family’s household budget and when aggregated for the entire nation. Utility incentives and government subsidies are helpful, but will never be enough to create a deep impact. Home energy improvements at the necessary volume and pace are not likely to happen without scalable, low-cost, energy-efficient mortgages to fund the purchase of new homes and to improve the efficiency of existing homes that Americans of all income levels can easily access.

Mortgages that Promote Energy Efficiency

Energy efficient mortgages (EEMs) can be obtained by borrowers to purchase or refinance an energy-efficient home or to pay for energy-efficient improvements in an existing home. They have been available for decades but their use has been distressingly low. According to David Heslam, executive director of Earth Advantage, a nonprofit that promotes construction and adoption of energy-efficient homes, several factors account for this lack of engagement:

- the addition of one more step to the overall stress and uncertainty of the home purchase process

- the difficulty in motivating a new buyer to take action on issues for which they have yet to encounter

- the lack of an incentive structure and perceived complexity for real estate agents and lenders to actively promote the use of an EEM.

Other forms of green financing that promote energy-efficient homes, such as PACE loans , are available in addition to EEMs. The biggest challenge with all of them is the lack of a robust mechanism for processing and approving them in the secondary mortgage market.

Secondary Mortgage Market

Although largely unknown to retail home buyers, the secondary market for home mortgages operates in the background to keep money available for home mortgages. Mortgage Backed Securities (MBSs) are financial instruments that allow local mortgage lenders to provide funds for home purchases by bundling many mortgages into bonds that are sold to investors or to Fannie Mae or Freddie Mac (the federally-backed home mortgage corporations). The proceeds are used to fund more mortgages, and the cycle continues.

Status Quo Solutions Aren’t Working

At present, the mortgage lending industry and the secondary mortgage market offer scant recognition or support for the extra value of energy-efficient homes. The major obstacle to developing and implementing EEMs for new and existing energy-efficient residential properties has been that Fannie Mae and Freddie Mac have been reluctant to recognize the extra value involved in energy-efficient homes. If they systematically recognized this value, it would legitimize energy-efficient homes in the eyes of the lending industry and provide a tool to finance them on a huge scale. One tool for accomplishing this goal would be a new category of MBS specifically tied to the energy performance of the homes being financed, called a green MBS.

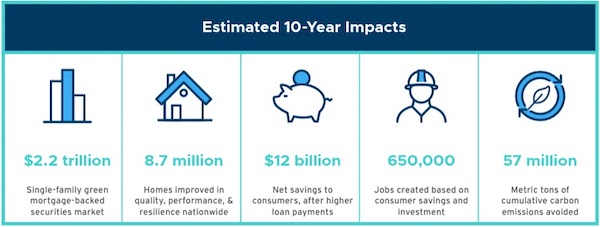

Green MBSs Could Invest Billions into Energy-Efficient Housing

According to Heslam, “Green MBSs for the existing home market can become a primary investment vehicle for deploying billions of dollars a year to home improvements that reduce residential emissions across the US. We recently collaborated with Rocky Mountain Institute on a report called Build Back Better Homes. ” The report, co-authored by Heslam, recommends changes in the secondary mortgage market and advocates for a nationwide uniform method for evaluating the energy efficiency of homes, along with a nationwide database that can be accessed by lenders in both the primary and secondary mortgage markets.

Fannie Mae currently has a conventional EEM, the Homestyle Energy Mortgage , while Freddie Mac offers the GreenChoice Mortgage . Both organizations are developing expanded programs and guidelines to better capture the economic and environmental benefits of energy-efficient homes and then channel those green home mortgages into a massive new green bond market. The potential numbers identified in the RMI report are compelling:

(Source: RMI Build Back Better Homes)

To support the success of Fannie and Freddie improving their guidelines for energy-efficient mortgage valuation, there are two key components needed to unlock the market for green MBSs: verification of home energy efficiency and an easily accessible database that stores verification information.

Documenting Home Performance

A trustworthy way of documenting a home’s energy performance or carbon impacts is critical to being able to qualify for a green mortgage and get successfully bundled into a green MBS. For existing homes, the U.S. Department of Energy’s Home Energy Score ™ is one good option and is positioned to be a consistent metric for use in every corner of the country, regardless of regional climate or local housing stock. The HERS Index is another viable rating system available nationwide. Earth Advantage is already working with USDOE along with local and state governments to ensure that home performance rating systems become a more regular part of real estate transactions. These tools provide an objective basis for properly valuing energy-efficient homes so they can qualify for EEMs and the green MBSs.

Capturing, Storing, and Transmitting Home Performance Data

To qualify mortgages and bundle them into green MBSs, Freddie and Fannie need a way to quickly verify this home performance information. That can be provided by a green building database that makes home energy performance ratings and certifications publically available. Fortunately, that database exists.

“Earth Advantage’s Green Building Registry ® is the largest single source of home performance information in the country and can be the conduit between energy-efficient homes and the secondary market’s financial products,” said Heslam. The Green Building Registry can be searched directly online and the data can be seamlessly transmitted to lenders and to local multiple listing services. This makes it easy to find validated, third-party verified green home data so that it can become integrated into lending, underwriting, and green MBS bundling processes.

Supporting Market Drivers

With a readily accessible metric to document homes with small carbon footprints and a clearinghouse to verify that information, Fannie and Freddie can more easily support higher loan amounts for energy-efficient homes and efficiently bundle these home mortgages to sell them as green MBSs to investors seeking environmentally beneficial investments.

This would create a built-in incentive structure for borrowers making green upgrades to their home or purchasing a new energy-efficient home. When Fannie and Freddie see market interest in green mortgages and the subsequent green MBSs, they could offer preferential terms, such as higher loan amounts, to borrowers either making home improvements or purchasing an already improved home. Green MBSs would support higher loan-to-value ratios for energy-efficient properties that could qualify additional buyers that find themselves on the margin. It would support the overall market for energy efficiency — allowing people to finance energy-efficient home purchases or energy improvements for their existing homes.

“For single family homes the primary benefit is that the home will be valued in its as-improved state and the loan-to-value ratio will be recalculated accordingly,” explained Heslam. “This is a particular value to a homeowner when it brings them up to 20% equity, for example. That homeowner does not need to pay mortgage insurance — a great relief.”

Green MBSs create a market-based incentive toward energy-efficient housing with the potential to influence consumer behavior in a way that surpasses the impact of traditional direct incentive payments to homeowners. “By building the hidden infrastructure that supports the development of green MBSs, we’re creating conditions that benefit homeowners directly, even though they may not be aware of it,” said Heslam. “Just as important, this infrastructure drives the mortgage industry in a direction that supports healthy, energy-efficient homes.”

Loans for Low Income Families

Expanding access to green capital must include a place for low-to-moderate income households and underserved communities to access benefits while being protected from harm. Through their Duty to Serve plans, Fannie Mae and Freddie Mac are obligated to address this issue by facilitating a secondary market for mortgages on housing for low-to-moderate income families in three underserved markets: manufactured housing, affordable housing preservation, and rural housing. As Fannie and Freddie expand their green mortgage and green MBS efforts, they must serve these families as well. And the fact that green MBSs will result in higher loan-to-value ratios for energy-efficient properties will help more lower income people qualify.

Why this Time Is Different

“We have to acknowledge that lending for energy efficiency and clean energy improvements has historically been challenging,” said Heslam.

He cites the recent experience with efforts like residential PACE lending. It has produced some good outcomes (including financing more than 300,000 home upgrades), but this success was too frequently achieved through high cost/low savings energy measures and predatory lending practices. A recent report on residential PACE in Missouri underscored that a poorly crafted and regulated lending program can have adverse impacts within more vulnerable communities.

Based on this experience, strong regulatory oversight, publically accessible third-party validation, and seamless distribution of building energy-efficiency data must be part of any financing protocol to ensure that the activity is truly producing financial, social, and environmental benefits. Organizations like Rocky Mountain Institute and Earth Advantage are leading the way along this new path. For more information on ways to support mortgages that promote energy efficiency and green MBSs, contact David Heslam at Earth Advantage .

Heslam explains that the timing couldn’t be better — now that investor interest in environmentally beneficial investment products is growing exponentially and there is a cascading incentive to develop the supply to meet that new demand. In this new investment context, verified and valid green mortgages become a valuable commodity that will be sought in numbers not seen at any time in the past. This investor demand creates the opportunity to scale a market-based incentive for home improvements that have documented energy and carbon reduction benefits.

“Paired with existing (and future) utility and government incentive programs, we feel that the U.S. is set to finally and comprehensively take on the problems inherent in our country’s carbon intensive housing stock ,” said Heslam. “These mortgages will not be the device that convinces homeowners to make energy improvements, but they will be the most secure and affordable way for the homeowner to pay for those improvements.”

And in this fast changing financing market, we can all do our part. As local lenders may not always be up to date with improvements with Fannie and Freddie’s policies, we can all move the availability of green mortgages forward by encouraging our lenders to use the energy-efficient financing tools already available. And we can encourage them to adopt new opportunities for energy-efficient lending that will soon become available.